Every founder knows the moment: the heart pounds, the palms sweat, and the potential of your life’s work hinges on a single, compelling presentation. That presentation is your pitch deck, and it’s arguably the most critical document you’ll create. It’s not just a collection of slides; it’s a strategic narrative designed to captivate investors and unlock the funding you need to scale your vision.

But what separates a mediocre deck from a winning pitch deck? It’s a precise blend of clarity, compelling data, and a powerful story. In this guide, we’ll break down the essential components—the very anatomy—that successful startups use to secure their funding rounds.

1. The Foundation: Setting the Stage (Slides 1-3)

A winning pitch deck must grab attention immediately and establish its core value proposition.

- Title Slide: Simple, professional, and memorable. Include your company name, a compelling high-level statement (your “North Star”), and your contact information.

- Problem: Define the pain point you are solving. This is not about your product—it’s about the market’s need. Use relatable examples and concrete numbers to illustrate the scale and urgency of the problem. If there’s no big problem, there’s no big business.

- Solution: Introduce your product or service as the logical, elegant answer to the problem. Be concise. What do you do? How does it fix the problem? Focus on the benefits to the customer, not just the features.

2. The Core: The Engine of Your Business (Slides 4-7)

This section proves your concept isn’t just an idea—it’s a viable, functioning business.

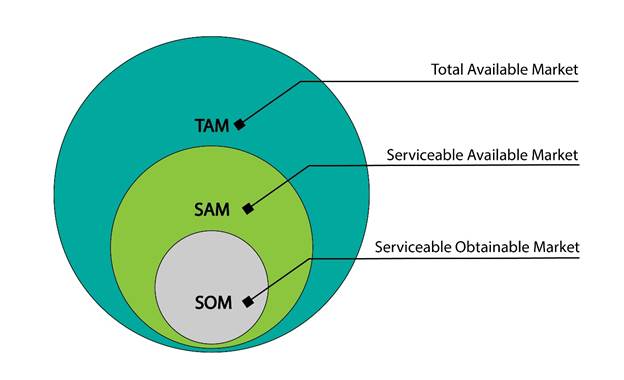

- Market Size (TAM, SAM, SOM): Investors want to know you’re playing in a large, growing sandbox.

- Total Available Market (TAM): The total market demand for a product or service.

- Serviceable Available Market (SAM): The segment of the TAM targeted by your products and services that is within your geographical reach.

- Serviceable Obtainable Market (SOM): The portion of SAM you can realistically capture.

- Tip: Use the “bottom-up” approach (based on customer data) rather than just the “top-down” approach (based on industry reports) to demonstrate a stronger grasp of reality.

Shutterstock

- Product/Service: This is where you bring your solution to life. Use clear screenshots or a very brief, high-level workflow diagram. Focus on the core value and competitive advantage. Avoid getting bogged down in technical jargon.

- Business Model: How will you make money? Outline your pricing strategy, revenue streams (e.g., subscription, transaction fee, advertising), and customer acquisition cost (CAC) vs. customer lifetime value (LTV).

3. Traction: Proving the Hype (Slides 8-10)

Data is the ultimate convincer. Traction slides separate the dreamers from the doers.

- Traction & Milestones: Show what you’ve accomplished to date. Use charts and graphs to illustrate growth in key metrics:

- Monthly Recurring Revenue (MRR)

- Number of active users

- Customer retention rates

- Successful pilot programs or partnerships

- Financials (Projections): Provide a three- to five-year forecast. Be realistic, but demonstrate a path to significant scaling and profitability. Highlight key assumptions behind your revenue numbers.

- Competition: Don’t claim you have no competitors. Show a landscape of the existing alternatives and clearly articulate your unique differentiation (the “secret sauce”) and sustainable competitive advantage (e.g., proprietary tech, network effects, data moats). A simple 2×2 matrix can work well here.

4. The People and The Ask (Slides 11-13)

Investors fund great ideas, but they bet on great teams.

- Team: Highlight the core team members, emphasizing their relevant experience, past successes, and why they are uniquely qualified to execute this specific vision. Investors are looking for passion, expertise, and complementary skills.

- The Ask (and Use of Funds): Clearly state the total amount of funding you are seeking (e.g., “$1.5 million Seed Round”). Crucially, detail how you plan to use this capital (e.g., 50% Product Development, 30% Sales & Marketing, 20% Hiring). This demonstrates fiscal responsibility and a strategic plan for the next 12-18 months.

- The Vision/Call to Action: End with a powerful, inspiring statement about your company’s long-term potential. What does the world look like if your company succeeds? Reiterate your excitement and thank the investor for their time. Include a strong call to action for the next meeting.

Summary: Keep It Simple, Make It Powerful

A winning pitch deck is typically between 10 and 15 slides. Every slide must earn its place by addressing an investor’s core questions: Is the market big? Is the team capable? Is the product defensible? Are the numbers convincing?

Master the anatomy, hone your narrative, and you will build a pitch deck that not only opens doors but secures the funding that transforms your startup vision into a market reality.

Who we are: Funded.com is a platform that is A+ BBB accredited over 10+ years. Access our network of Angel Investors, Venture Capital or Lenders. Let us professionally write your Business Plan.